Economic policies

Taxation of electric company cars: The measures bear fruit

Since the start of 2019 the tax rate for electric vehicles has been halved. The same year saw the number of newly registered electric company cars more than double. We should retain the existing rules.

- Topics

- Economic policy

- Taxes

- Taxation of electric company cars

Taxing company cars

The current taxation of the private use of company cars according to the "1% method" is correct and has proven itself in practice.

Current legislation in 2021

- Normal case: Flat-rate calculation according to the 1% method. For the flat-rate taxation of the private use of company cars, 1% of the gross list price at the time of initial registration of the vehicle is to be applied per calendar month, the so-called 1% method. Vehicle use for trips between home and the first place of work is additionally assessed at 0.03% of the gross list price per kilometer.

- Alternative: Log book. Instead of the flat-rate calculation of the private share (1% method), the employee/entrepreneur can also determine private use by itemizing all journeys and the total costs. This requires the employee/entrepreneur to keep a precise logbook showing the total mileage for business and private use in each calendar year. The total costs plus VAT of the vehicle are then divided into a business and private share in proportion to the kilometers driven.

- Privileges for electric vehicles (BEV, PHEV): For the taxation of the private use of electric and hybrid electric vehicles purchased as company cars after December 31, 2018, and before January 1, 2031, the gross list price used for the 1% method is reduced by half. PHEVs will need to meet additional requirements that tighten over time to remain eligible. For BEVs purchased from 2020 onwards with a gross list price of up to €60,000, the assessment basis for applying the 1% method will also be reduced to a quarter of the gross list price from the 2020 assessment period onwards. When applying the logbook method, the depreciation to be taken into account is also to be halved or quartered accordingly. (-> Verweis auf Artikel „Besteuerung der Elektromobilität“)

- Economic significance: The percentage of company cars among all new passenger car registrations reached a new high of 39.3% in 2022, up from 28.9% in 2010. Of the 2.65 million new passenger car registrations in 2022, 1.04 million were company vehicles.

The halving of the tax base for BEV/PHEV/FCEV introduced at the beginning of 2019 is effective. In 2019, the increase in new registrations of electric passenger cars as company cars accelerated sharply by +107%; in 2018, this increase was still only 13%. In 2020 the growth rate accelerated even further and reached +225 %. We therefore expressly welcome the extension of the subsidy for electric vehicles until 2030, introduced at the end of 2019 with the Act on Further Tax Incentives for Electric Mobility. It represents a worthy contribution to the further ramp-up of e-mobility. The gradual change to the criterion for the range of PHEVs provided for in the EStG is already accompanied by a steady tightening of the regulation.

We reject recurring considerations aimed at placing internal combustion engines (ICEs) with high CO2 emissions at a disadvantage. There are several reasons why this is not the right approach. On the contrary, the current regulation on company car taxation is a flat-rate calculation that realistically reflects the average percentage of total costs accrued on purely private trips. It is constitutional and has proved itself in practice, and, as such, it should be retained. Tightening it would violate fundamental principles of tax law.

Legal typifying according to the 1% method justified

Typifying and flat-rate regulations are constitutionally justified mainly for reasons of practicability and administrative ease.

- The 1% method is constitutional: The gross new list price serves as a generalized basis for assessing the value of the benefit of use based on the typified new acquisition costs (simplification by dispensing with individual records and proof).

Company car taxation not a subsidy

The current regulations do not have a subsidizing character as they are in line with reality and the calculated financial advantage from private use is not set too low. It is therefore not a privilege. Similarly, the taxation of the private use of a company car does not constitute a subsidy within the context of Section 12 of the Economic Stability and Growth Law (StabG). Rather, the value of private use determined at a flat rate of 1% of the gross list price realistically reflects the average percentage of total costs attributable to purely private journeys and the underlying standard case accurately reflects the typical financial advantage.

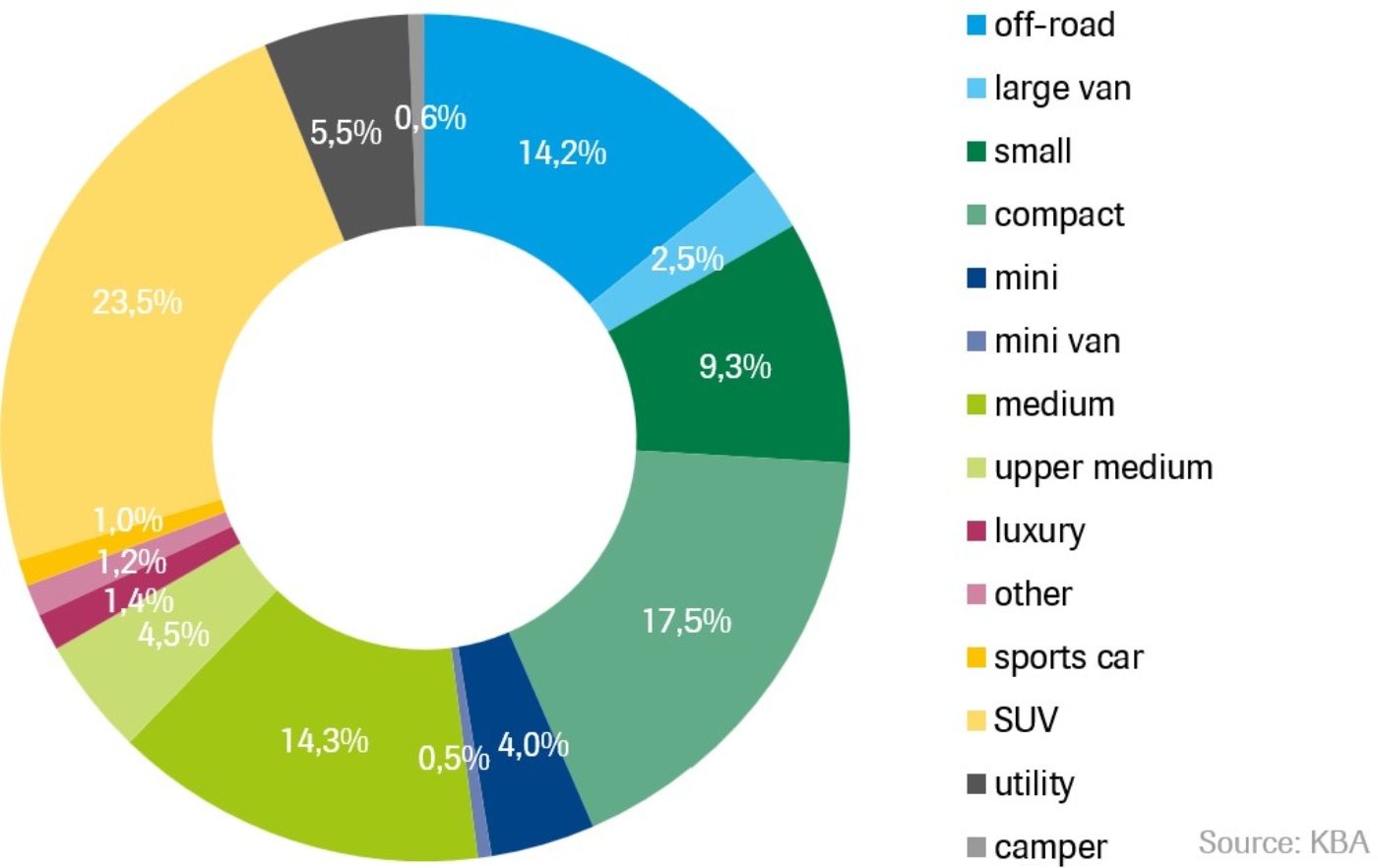

Only a small number of company cars are luxury class

Among all new registrations, around 46% of all company cars are smaller vehicles (mini cars, small cars, minivans, compact and mid-size vehicles). The share of the luxury class, on the other hand, is just 1.4%.

Contact person

Dr. Karoline Kampermann

Head of the Economic Policy and Taxes Department